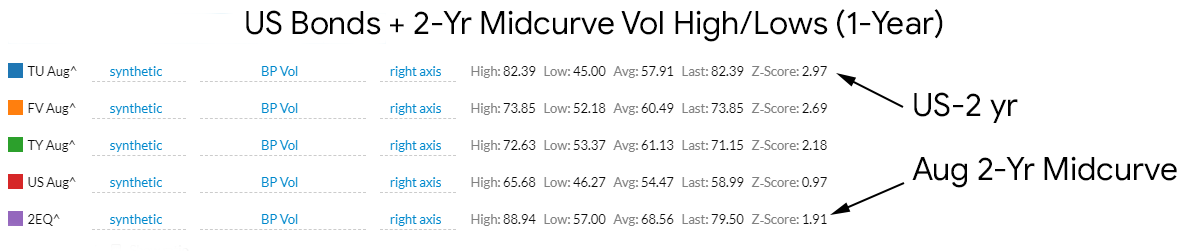

If you’re following the US Bond complex you will have seen the recent spike in US-Year 2-Yr Bond Vol relative to the other contracts.

Checking the 2-Year Midcurve Options for a good match to the US 2-Yr Bond Aug expiry, the 2-Yr Midcurve August expiry in 78 days versus Bond expiry in 57 days looks good value, which should give a vega weighted credit and extra days on a switch.

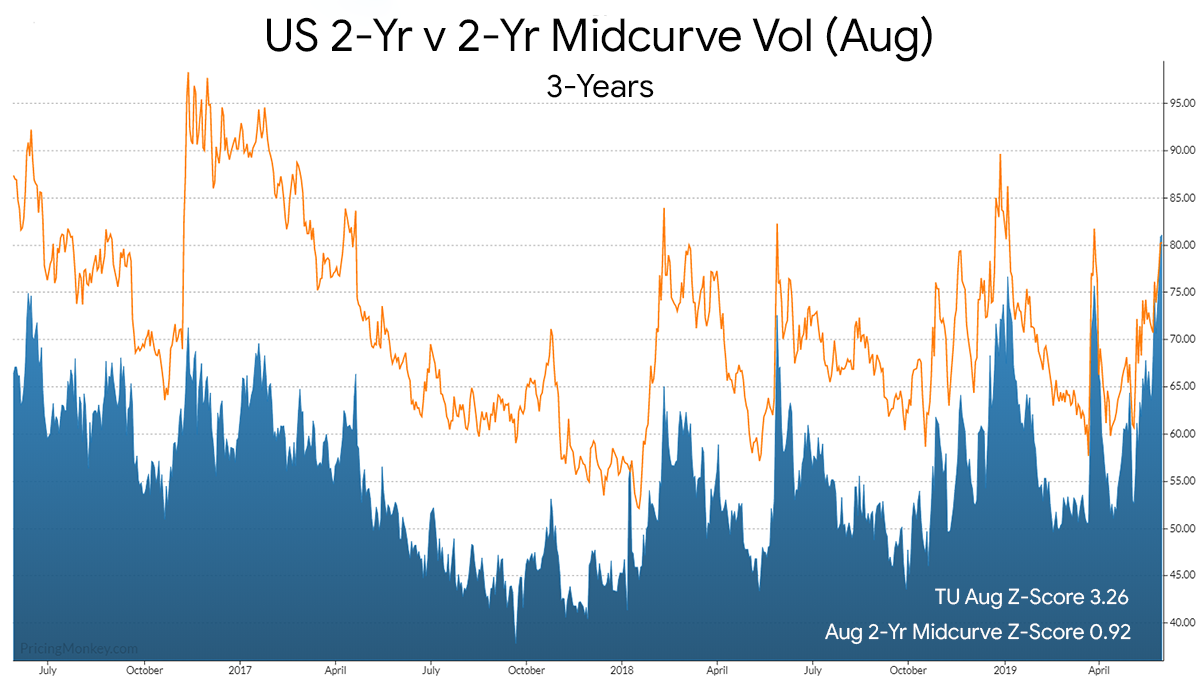

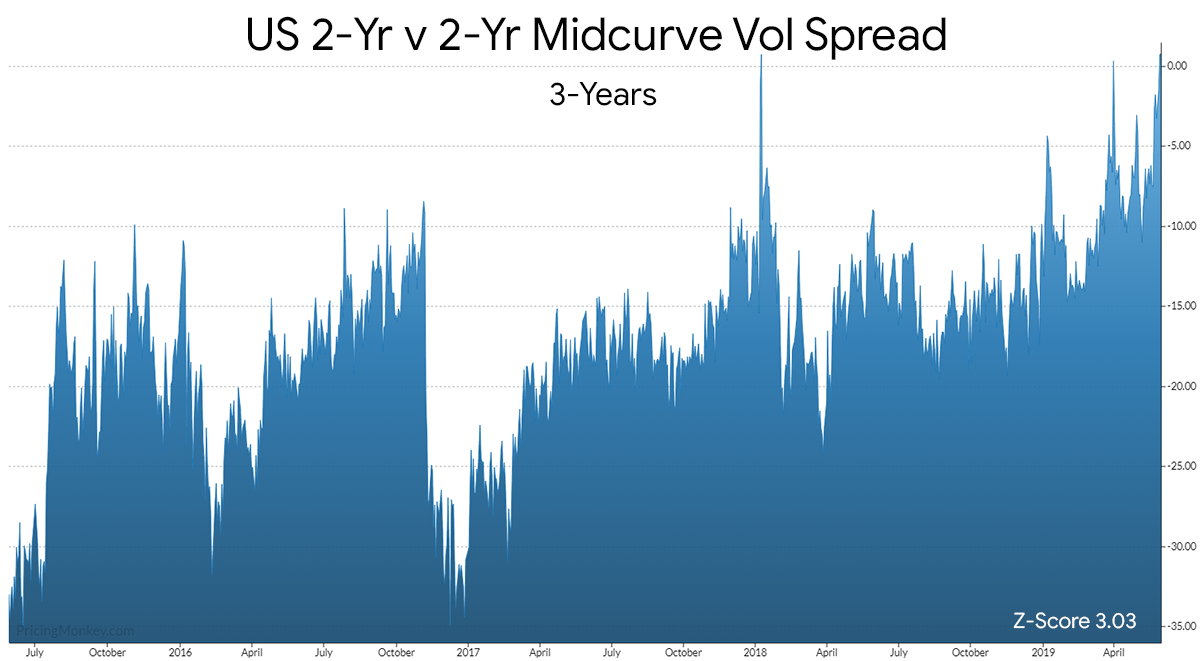

The spread history clearly shows how unusual this move is.

Example of vega weighted potential switch.