Sell June ED 98.50 Straddle @ 20.5 with 122 days to expiry

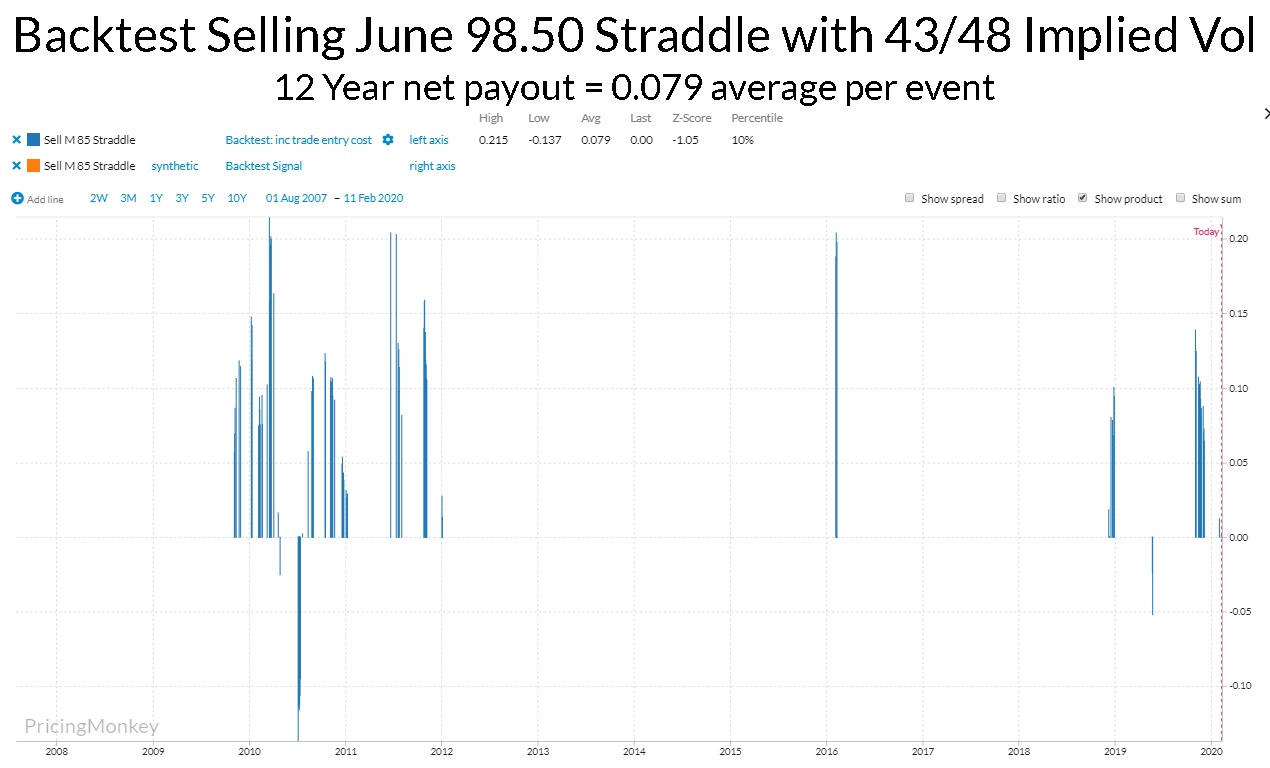

This has been trading at 20.5 ticks this afternoon, which looks around 44 Implied Vol. Backtesting shows that selling 122 day straddles with only a 43/48 Implied Vol Range would have returned 7.9 ticks net over the last 12 years on average per trade.

In addition, the trade looks high on Percentile (84%), and payouts look reasonable for current market conditions.

As you can see Vol up here is pretty rare for this June Straddle(122 day). Encouragingly the trade idea did very well back in 2009/2012.

Trade booked for tracking.