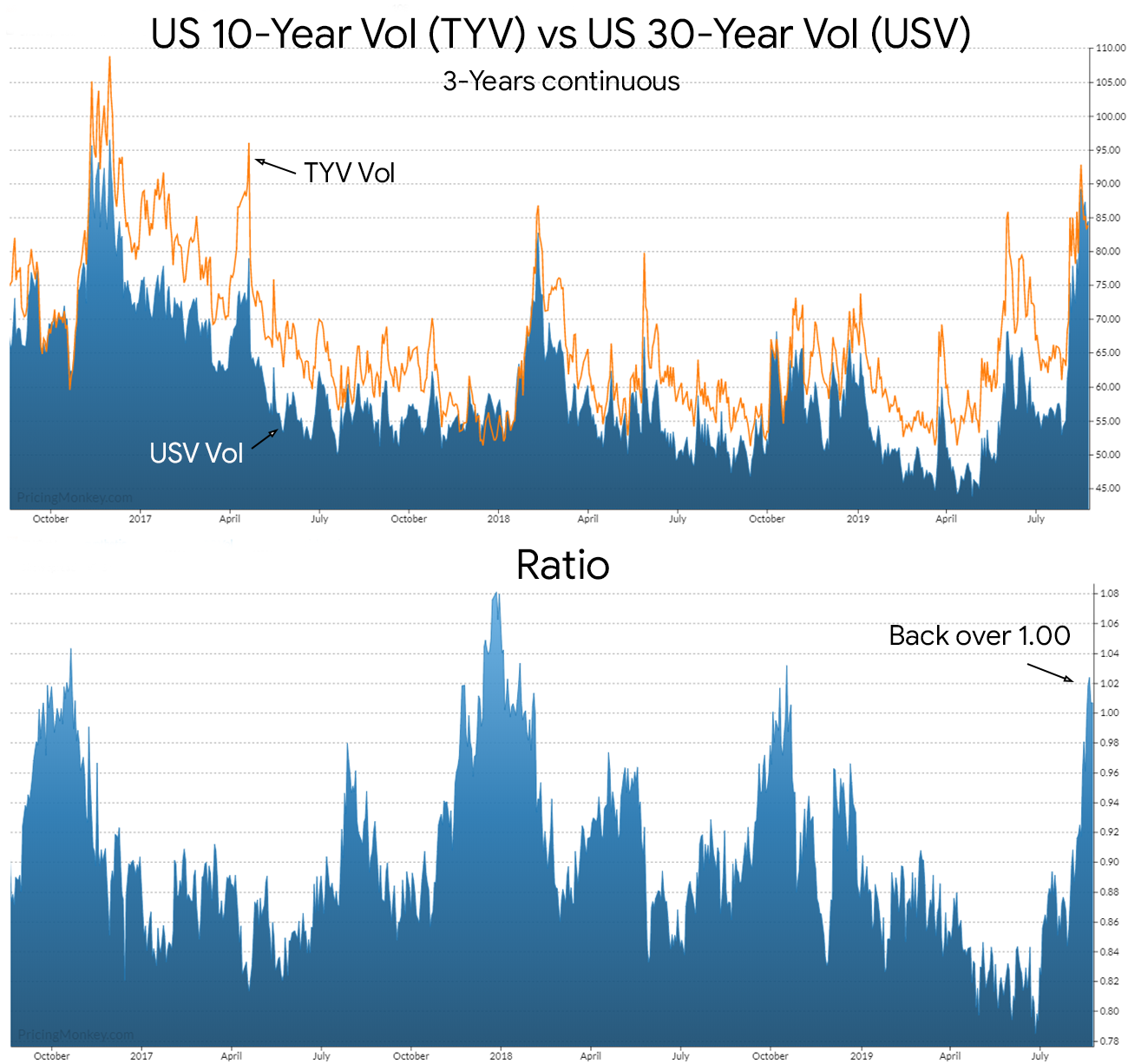

oct19 us t-bond 164.00 straddle vs oct19 10y note 131.00 straddle

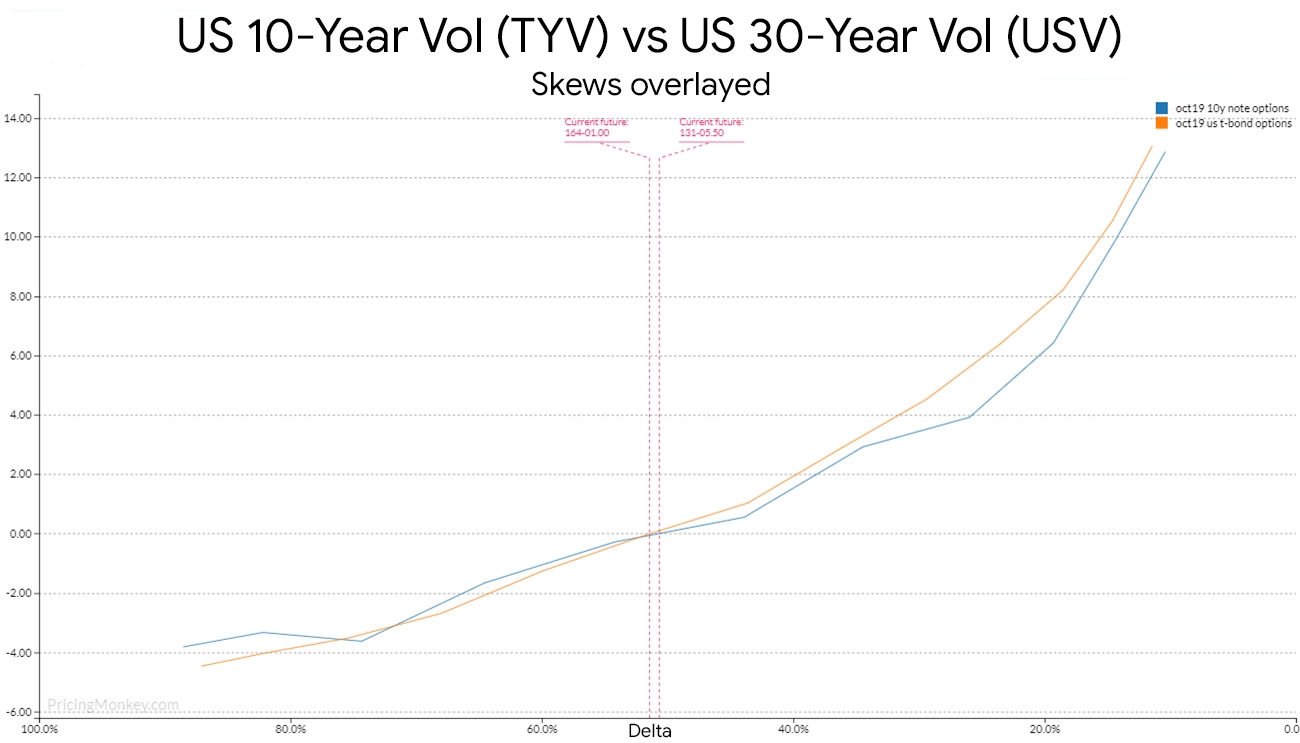

The Implied Vol play between USV and TYV looks to be at an interesting level that might be worth a look. Also, the skew on both contracts is pretty similar, so if you have a view on the 10’s/30’s curve here, the similar Vol might be useful for directional trading ideas.

Skew delta overlay

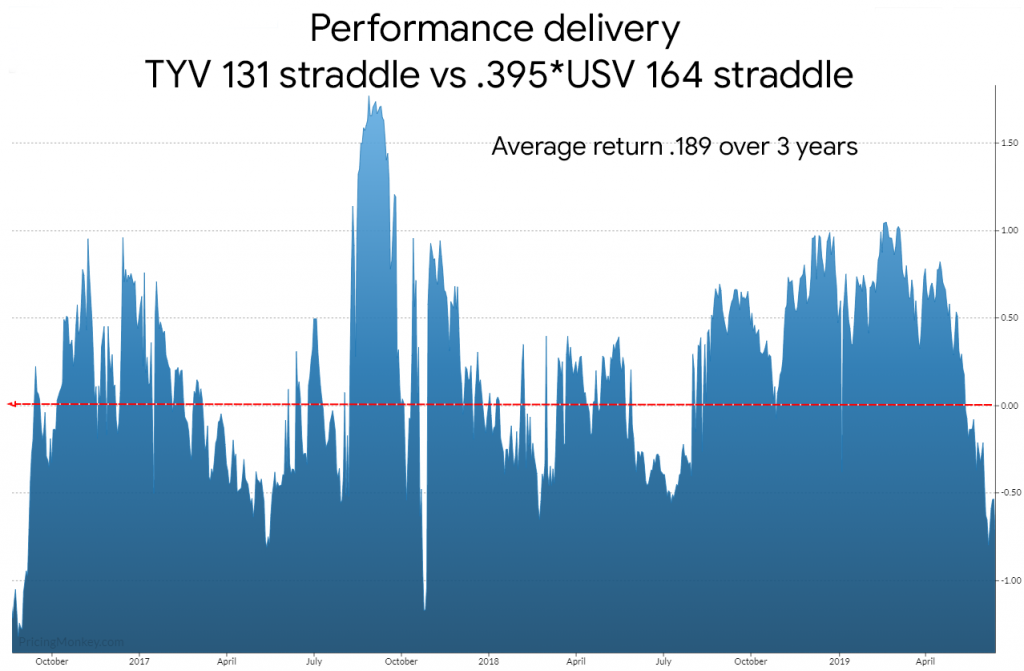

Performance (beta feature)

Trade returns .189 (decimal) over 3 years, obviously it’s very exposed to 10’s/30’s curve moves, hence the swings.

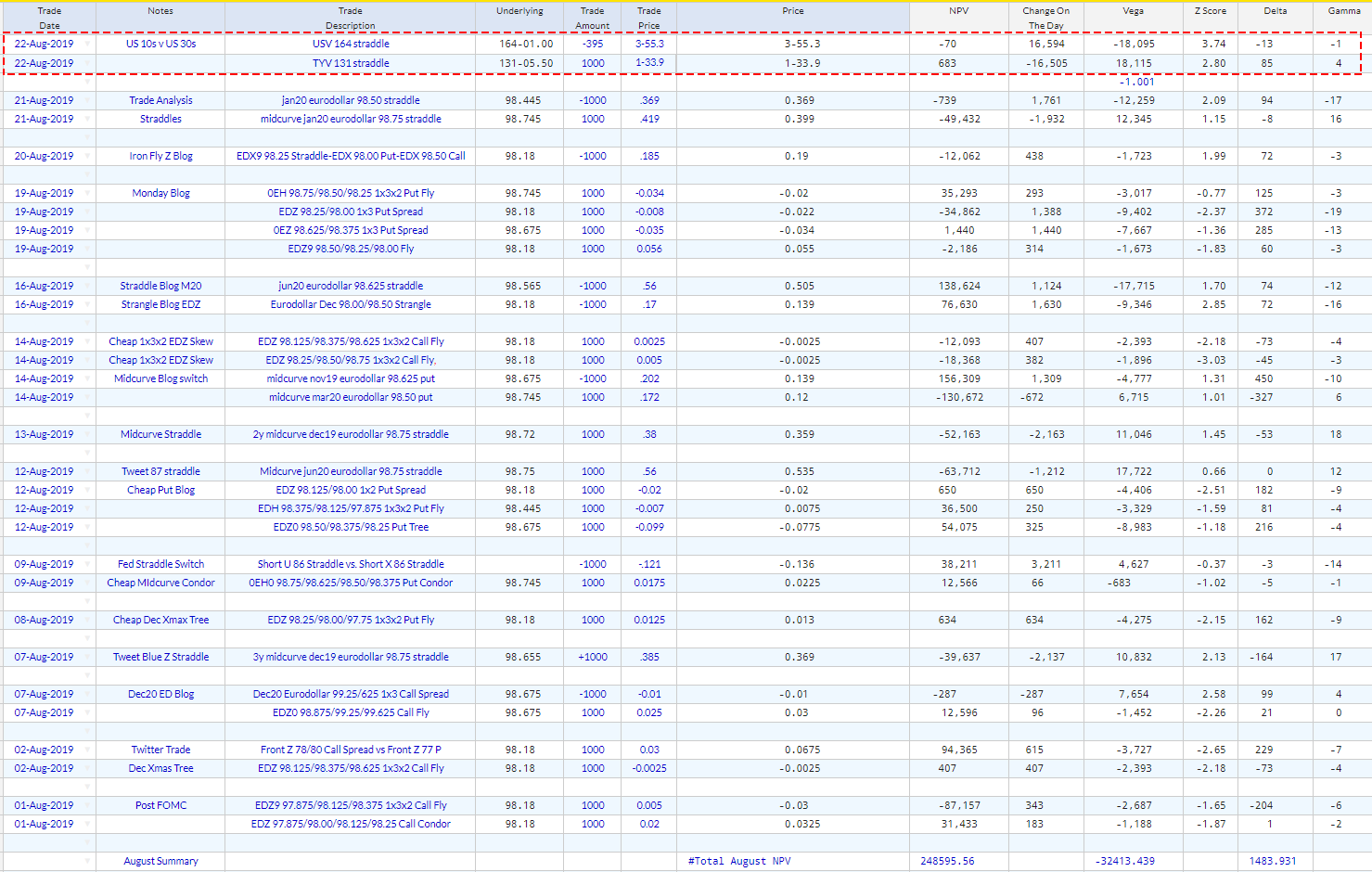

Trade booked for monitoring, we used vega for hedge amounts