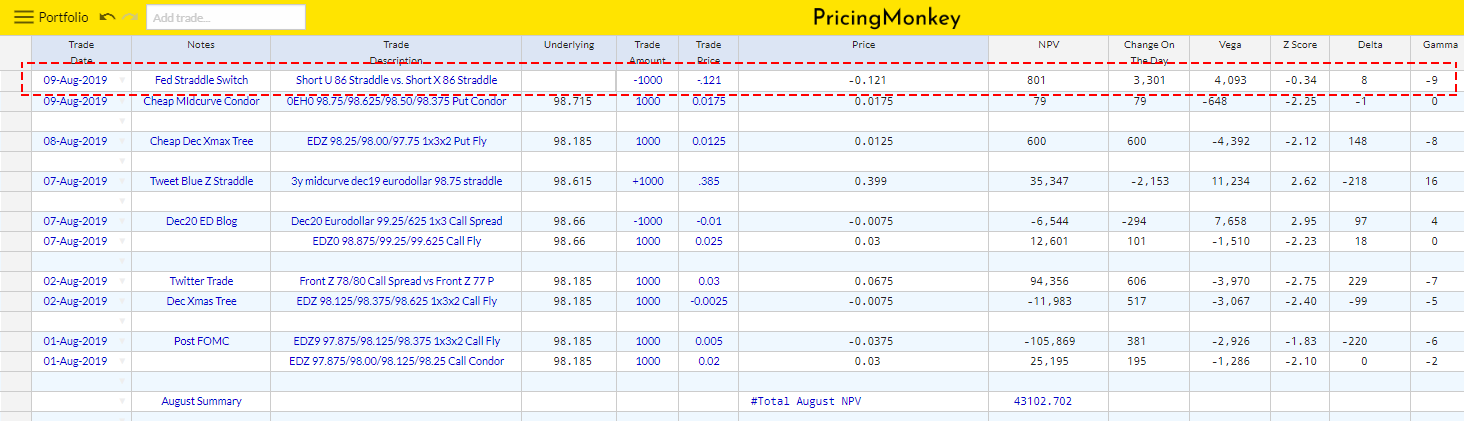

Spotted this trade going through the market earlier, Short U 86 Straddle vs. Short X 86 Straddle

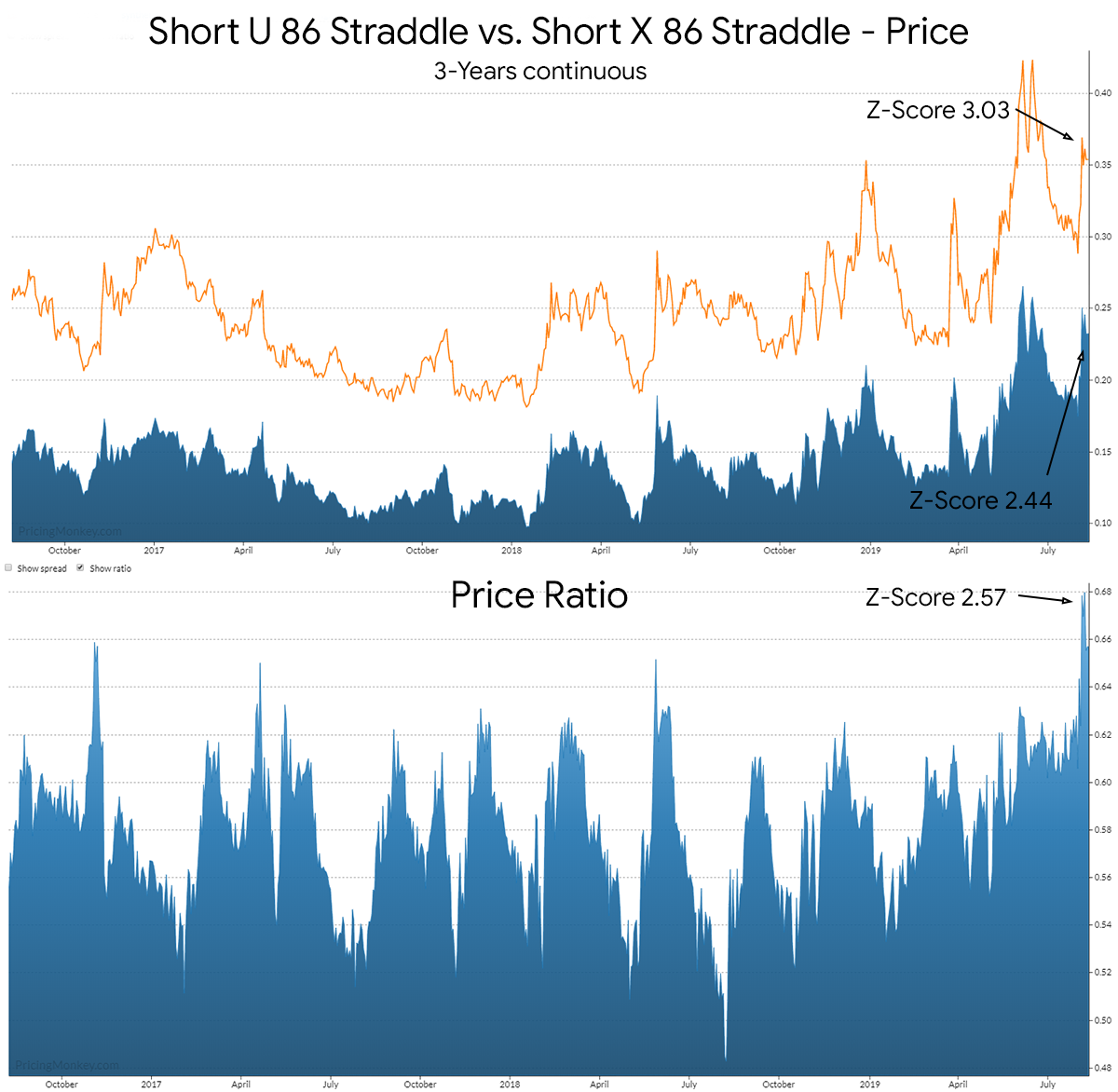

Taking a closer look in PricingMonkey at the history of the 2 synthetic contracts (Short U 86 Straddle vs. Short X 86 Straddle) in price terms clearly shows how the Sept Vol over Nov Vol is impacting the prices. Sep’s price ratio is 68% of Nov currently (lower chart). Sep expires on the 13th Sep, 4 days ahead the the 17/18th Fed meeting.

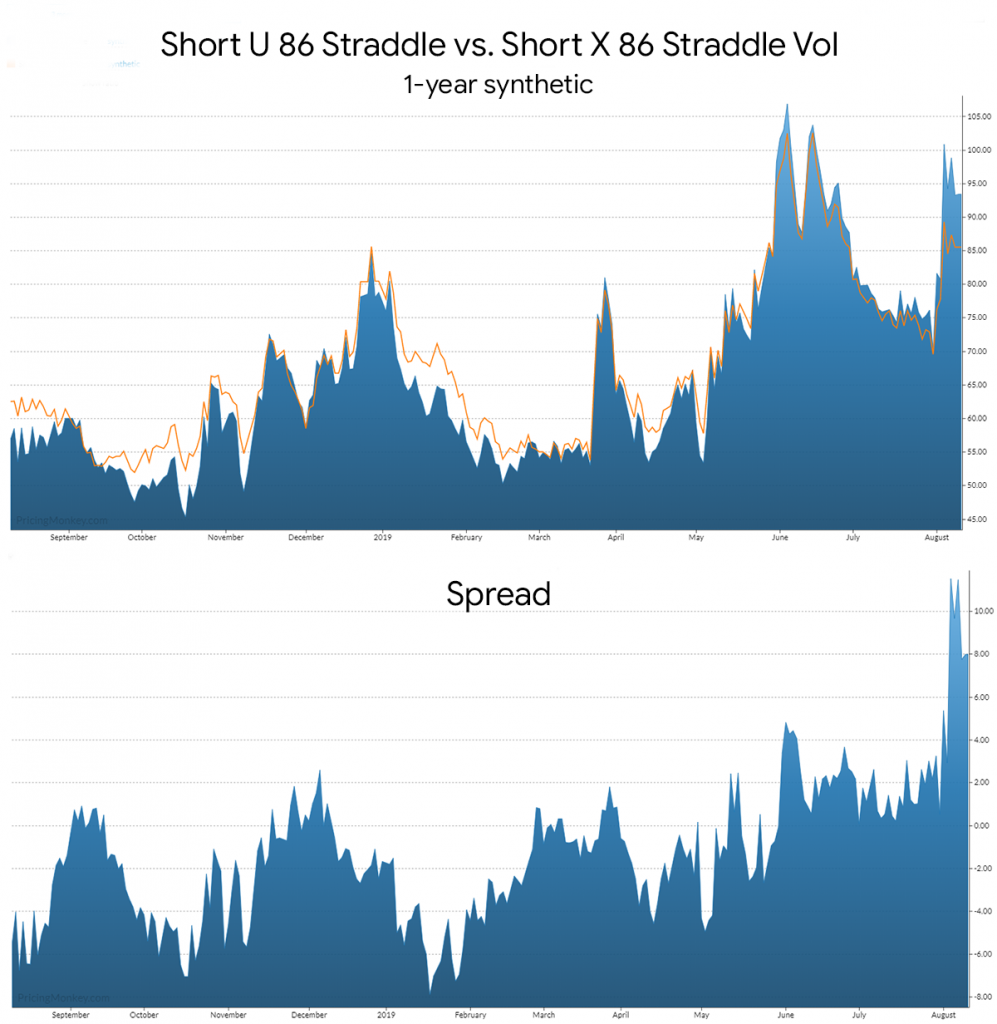

Vol view of each straddle

Trade booked for tracking.